The letter of credit is often equated with the documentary credit which it differs by the absence of advising and confirming bank.

This assimilation is an abuse of language that can cause confusion because in many cases the degree of credit risk coverage provided by the letter of credit is lower than the one provided by the documentary credit.

It is therefore important to know precisely the differences between the two tools and when one should be used rather than the other.

The documentary credit involves four players:

- The buyer's bank. This is the issuing bank

- The seller's bank. This is the advising bank and eventually confirming bank.

- The seller. This is the exporting company.

- The buyer. This is the importing company

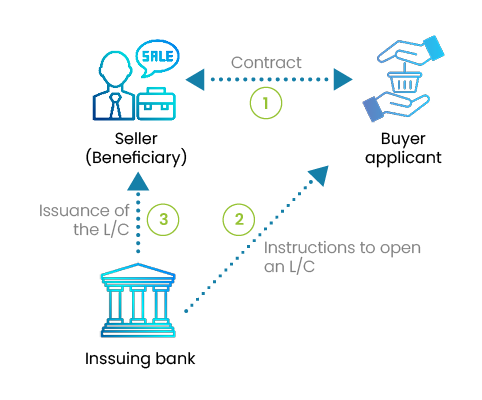

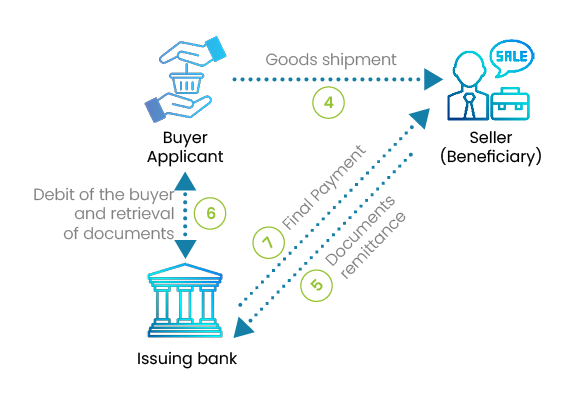

Letter of credit process

The liabilities of all the parties involved are defined by the Uniform Customs and Practices for Documentary Credit – UCP – ICC Publication 600.

The buyer's bank verifies the solvency of its customers as well as the signatures on the application form. It also ensures that the instructions are clear and complete.

Why involve a second bank (the case of documentary credit)?

In the case of the letter of credit, only the issuing bank is involved. The entire risk is therefore based on this bank. Will she honor its commitments? Can be there an arrangement with the buyer who is its client to the detriment of the seller? This is to avoid that risk that most exporters prefer to include their bank in the process and ask them to ensure the entire transaction (the bank is confirming in this case).

In fact, a letter of credit may be an acceptable solution if the issuing bank is a leading bank whose professionalism and impartiality are indisputable. Its advantage is to be much cheaper. Indeed, most of the cost of a documentary credit is the confirmation of the advising bank who handle de facto the entire risk.

The documentary credit will be preferred if there is a significant political risk in the country of the buyer. In this case, the confirmation of the seller's bank covers it against any non-payment because of a political event (war, embargo ... etc.) making the payment impossible to be done.

The letter of credit should not be confused with the standby letter of credit which is a bank guarantee of payment, but in no way a means of payment.