Trade receivables are a major issue for companies, their cash flow and profitability. They often represent a significant part of the assets of the balance sheet and therefore of the use of the financial resources available to the company.

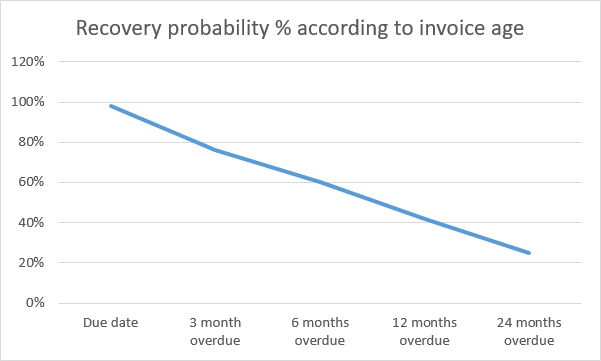

This current asset does not create value but depreciates with the passing time because the probability of recovering a debt decreases sharply after a few months overdue and because of inflation.

This principle applies whatever the situation or the type of debtor (administrations, companies in collective proceedings, key accounts ...). Indeed, if it is easy to understand a loss because of a company who went bankrupt, it seems less obvious but it is as much real to suffer an unpaid from an administration or a large company because of the complexity administrative process becoming inextricable with the age of the debt.

Companies are implementing many strategies to improve their AR management and reduce their debt-related working capital requirements:

Indeed, if it is easy to understand a loss because of a company who went bankrupt, it seems less obvious but it is as much real to suffer an unpaid from an administration or a large company because of the complexity administrative process becoming inextricable with the age of the debt.

Companies are implementing many strategies to improve their AR management and reduce their debt-related working capital requirements:

Whatever are the solutions choosen, they have a cost that must be put in perspective with the expected gains.

How to value the cost of the receivables, and therefore the potential gains resulting from the improvement of their management?

The answer to this question is not obvious. Putting it to specialists often results in as many different answers as respondents, which testifies to the subjectivity of the subject.

This current asset does not create value but depreciates with the passing time because the probability of recovering a debt decreases sharply after a few months overdue and because of inflation.

This principle applies whatever the situation or the type of debtor (administrations, companies in collective proceedings, key accounts ...).

- Optimization of payment terms granted to customers

- Implementation of a specialized software to improve the credit risk follow-up and the collection of the accounts receivable

- Use of credit insurance to secure this position and limit the risk of loss

- Hiring of business specialists (credit manager, collectors, credit analysts) or outsourcing this activity to BPO (Business Process Outsourcing) companies

- Factoring or other assignment of receivables tools.

- Mobilization of outstanding bills of exchange and other financing solutions (retro-factoring ...)

- ...etc.

How to value the cost of the receivables, and therefore the potential gains resulting from the improvement of their management?

The Weighted Average Cost of Capital and the Cost of Debt

1. Weighted Average Cost of Capital (WACC)

Some financial manager value the receivables with the weighted average cost of capital, which represents the global cost of financing of the company.

WACC calculation

Formula: (EQ x EQk + DML x DMLk + DST x DSTk) / (EQ + DML + DST + OD)

Details :

EQ: equity (EQk : cost of equity in %)

DML: debts medium & long term (DMLk : cost of DML in %)

DST: debts short term (DSTk : cost of DST in %)

OD: other debts (no cost)

For example, if the customer outstanding is an average of 5 million euros over the year, and the weighted cost of capital is 5%, the annual cost of the AR is 5 million x 5% = 250,000 euros.

This approach may be relevant for companies that do not have a cost of capital very different from the cost of debt, especially SMEs.

For the others, and particularly the companies listed on the stock exchange, the weighted cost of the capital is often very high because of the expected profitability of the shareholders, also very high.

In addition, these same companies obtain short-term financing at extremely low rates, even negative in the current environment favorable to low interest rates.

They can therefore offset a cash impact due to an increase in the customer item by a quasi-free short-term credit line. In this case, the weighted cost of capital can not be the right ratio to value the accounts receivable because it overstates its real impact on the profitability of the company.2. Cost of debt

Another solution is to use another ratio: the cost of the debt, corresponding to the weighted cost of the short-term and medium-term debts. The cost of capital (i.e. the cost of the shareholders) is therefore excluded from the calculation which greatly reduces the cost of the AR and makes it much more realistic.Calculation of the cost of debt

Formula: (DML x DMLk + DST x DSTk) / (DML + DST + OD)

Details :

DML: debts medium & long term (DMLk : cost of DML in %)

DST: debts short term (DSTk : cost of DST in %)

OD: other debts (no cost)

Equity is excluded from the calculation compared to the WACC.

Evaluate the Accounts Receivable with the Cost of Credit (CoC)

The principle of the CoC is to take into account all the elements that actually finance the Accounts Receivable: short-, medium-, long-term financial debts, other debts ... and the share of equity that finances the current assets, that is the working capital (Equity - fixed assets).

Thus, the cost of capital is taken into account but in fair proportion as well as all the other liabilities particularly financing current assets including receivables.

If working capital is negative, the portion of long-term debt that finances fixed assets is also excluded from the calculation.Calculation of the Cost of Credit

1. If working capital is positive:

Formula: (WC x EQk + DML x DMLk + DST x DSTk) / (WC + DML + DST + OD)

2. If working capital is negative:

Formula: ((WC* + DML) x DMLk + DST x DSTk) / (WC* + DML + DST+ OD)

* the WC is negative there

Details :

WC: working capital (equity - fixed assets) (EQk : cost of equity in %)

DML: debts medium & long term (DMLk : cost of DML in %)

DST: debts short term (DSTk : cost of DST in %)

OD: other debts (no cost)

It allows to put in perspective the cost of such a project with the real gains that it can bring and to avoid the validation of solutions whose profitability would be based on a too important valuation of the expected gains (based on weighted cost of the capital).

It is therefore an essential tool for the credit management strategy implemented in the company.