Downloadable tools are available at the bottom of the page

Economic history can be likened to the history of economic crises, which correspond to periods of accelerated transformation of the ecosystem and its constituent actors.

Depending on the nature of the crisis (health, political, technological, etc.), the effects vary, but one constant across all crises can be highlighted: some actors, particularly businesses, disappear, others transform, and still others emerge.

Crises can have a significant impact on the level of activity, with sudden shutdowns, restarts, changes in practices, etc.

In all countries that have been confined, the first effect was to reduce economic activity by around 40%, with a very variable rate depending on the activity sector. Thus, the construction industry showed a drop of 90% while rare sectors such as digital or online commerce enjoyed a certain stability or even an increase.

However, shutting down the economy did not immediately generate massive business bankruptcies.

State aid, through partial unemployment, guaranteed loans and deferral of charges have a very important buffer effect in some countries, all the more so that this situation considerably slows down the declarations of insolvencies and the judgments of insolvency proceedings.

From a credit analysis point of view, this context has a masking effect.

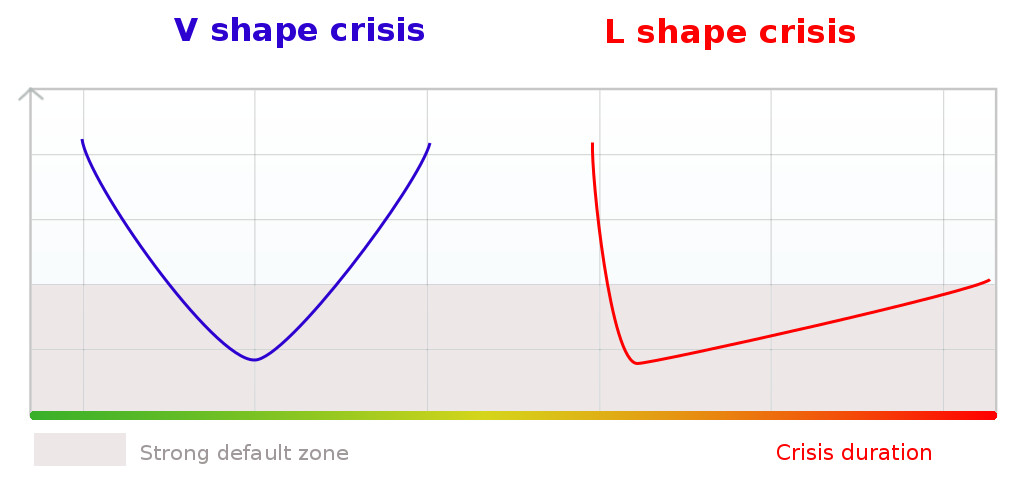

A company can be virtually insolvent, but the assumption or deferral of a large part of its costs by the state masks this reality until the end of these temporary measures. If the crisis is in a "V" shape (see diagram below), a sharp fall and then a rebound as powerful as the fall has been, it is likely that a large majority will manage to spread and absorb the shock.

Read The credit management facing a shock wave.

The problem stems from the high likelihood that the recovery will be slower and more difficult with an "L" crisis format, especially in countries where the confinement was strict like in western europe. As we can see in the diagram above, the area representing the zone of strong failures is much larger in this scenario.

Without a return to an activity of a level comparable to before the confinement, a company will have to both drag the financial burden of two months without turnover (external aid only covers part of the costs), and a significant drop in income in the months following this period. Many will not be able to cope with this double penalty without lasting liquidity support. This is what we can call "the long tail of defaults": the main part of defaults does not occur during the major fact of the crisis (confinement), but during the following months because of the direct consequences and indirect effects of this event.

A company getting public aid selling to other companies and experiencing a sharp drop in turnover may initially see its cash flow improve or at least be maintained. This seems paradoxical but is simply the result of a lag effect.

This is what we can call "the long tail of defaults": the main part of defaults does not occur during the major fact of the crisis (confinement), but during the following months because of the direct consequences and indirect effects of this event.

A company getting public aid selling to other companies and experiencing a sharp drop in turnover may initially see its cash flow improve or at least be maintained. This seems paradoxical but is simply the result of a lag effect.

If you continue to manage your outstandings and your credit analyzes as before, you will be like a collection officer carrying out his scores and reminders on Excel in the age of integrated web credit management solutions: exceeded in efficiency and results.

The great peculiarity of this crisis is its suddenness. A creditworthy business before lockdown begins can be in agony a few months later. In other words, if you set a credit limit and payment terms on the basis of the 2019 balance sheet which has just been published, you are likely to miss the point. Faced with this risk of extremely rapid deterioration, it is essential to change your approach in order to have a realistic perception of your clients' financial situation and to make your choices with full knowledge of the facts.

For this, count above all on yourself and the information and the deductions that you can make.

Indeed, mass financial information providers will be lagging behind at least for some time. No algorithm is able to assess in detail the effects of this crisis, which are different for each sector but especially for each company.

As for credit insurers, they are obliged to massively restrict their commitments by making large cuts in the guarantees granted, and this, with few possibilities of doing it on a case-by-case basis. The information collected through the amount of the guarantee thus loses its quality while credit insurance cost increases. Committed to hundreds of billions of euros, credit insurers could not support a default rate of even 1% of the sum of guarantees granted. It is therefore natural that they retract during these periods of great uncertainty and increasing risk. They also must survive the crisis.

The guaranteed inquiry appears to be relevant in this context. Indeed, it is based on an in-depth financial report which was produced by an expert credit analyst with specific and complementary sources of information.

The information obtained directly from customers via telephone follow-up actions in particular and the monitoring of their payment behavior with your company are the first indicators to be taken into account because they are the most immediate, specific and the most factual. If financial analysis no longer makes possible to assess the short term solvency of companies, it remains relevant for estimating their resilience to the crisis.

Indeed, it is obvious that a solid structure having accumulated cash reserves will have more capacity to absorb the shock than those which usually operate in just-in-time

It is therefore the combination between:

This is why the analysis focuses on simplified information. They can be obtained during a telephone conversation and an analysis of the n-1 financial statements. Rather than focusing on details and spending a lot of time on an assessment, credit analysis aims to understand the "great masses" and synthesize them to arrive at a credit decision. With experience, a quick zoom is made on the few points of the balance sheet which have drawn attention. Necessary time ? 5 to 10 minutes is sufficient for an experienced person when the required information is present.

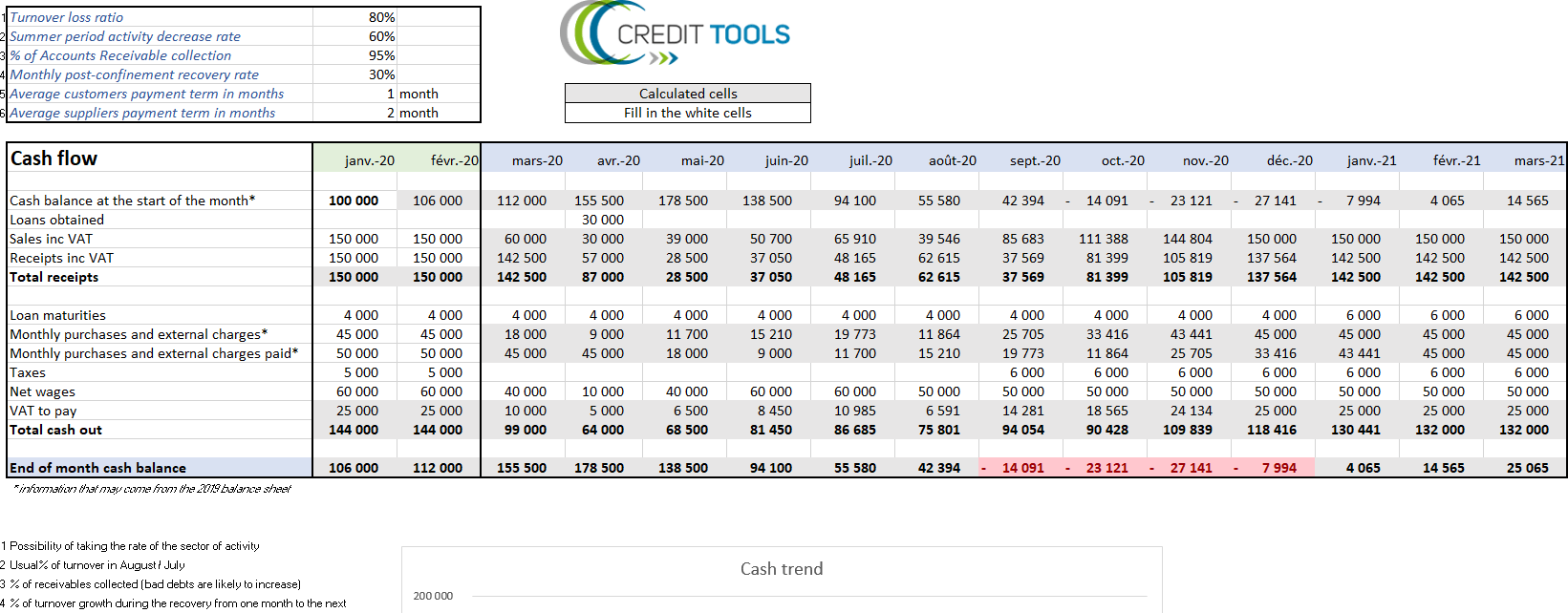

The principle is simple and similar to a cash flow forecast but incorporating the peculiarities of the crisis: the often sudden stop and the aid got from government.

Download the Excel file to perform this cash flow evolution simulation according to the above criteria.

In many cases, it highlights the time lag between the cause (containment) and the effect (possibly negative cash flow) and the better resistance of companies with a high level of liquid current assets (receivables, cash, etc. .).

At the macroeconomic level, it is likely that the increase in insolvencies will be significant, especially in following years.

Periods of severe crisis increase the risk of non-payment even though these can be significantly reduced depending on the terms and methods of payment granted and the guarantees obtained.

It is appropriate for each company to define the part of the risk that it accepts to take with each client by applying its credit management strategy which must be rethought and adapted to the situation.

The most important thing is to make choices in full knowledge of the risks involved and according to the objectives and the capacities of your company to absorb a certain level of customer risk. Thus, the analysis carried out can lead to either demanding very restrictive payment conditions or the setting up of support aimed at helping his partner to overcome this difficult phase.

In the latter case, it is relevant to ensure that you are not the only supplier to help the company in question and to enter into contractual arrangements for the facilities granted in order to specify reciprocal commitments.

Depending on the nature of the crisis (health, political, technological, etc.), the effects vary, but one constant across all crises can be highlighted: some actors, particularly businesses, disappear, others transform, and still others emerge.

Crises can have a significant impact on the level of activity, with sudden shutdowns, restarts, changes in practices, etc.

The Covid 19 example

The economic crisis following the Covid 19 health crisis is different from any that we have experienced before. Large swathes of the economy have never been brought to a halt in modern history.In all countries that have been confined, the first effect was to reduce economic activity by around 40%, with a very variable rate depending on the activity sector. Thus, the construction industry showed a drop of 90% while rare sectors such as digital or online commerce enjoyed a certain stability or even an increase.

However, shutting down the economy did not immediately generate massive business bankruptcies.

State aid, through partial unemployment, guaranteed loans and deferral of charges have a very important buffer effect in some countries, all the more so that this situation considerably slows down the declarations of insolvencies and the judgments of insolvency proceedings.

From a credit analysis point of view, this context has a masking effect.

A company can be virtually insolvent, but the assumption or deferral of a large part of its costs by the state masks this reality until the end of these temporary measures. If the crisis is in a "V" shape (see diagram below), a sharp fall and then a rebound as powerful as the fall has been, it is likely that a large majority will manage to spread and absorb the shock.

Read The credit management facing a shock wave.

Patterns of sudden crises

The problem stems from the high likelihood that the recovery will be slower and more difficult with an "L" crisis format, especially in countries where the confinement was strict like in western europe. As we can see in the diagram above, the area representing the zone of strong failures is much larger in this scenario.

Without a return to an activity of a level comparable to before the confinement, a company will have to both drag the financial burden of two months without turnover (external aid only covers part of the costs), and a significant drop in income in the months following this period. Many will not be able to cope with this double penalty without lasting liquidity support.

Indeed, the reductions and deferrals of charges are almost immediate, while the drop in receipts from customers will be delayed by 60 days on average according to the country payment profile (if it effectively manages its collection, of course).

However, the boomerang effect will be violent because few months later, collections will drop in proportion to the drop in turnover, while expenses will return to their usual level.

What are the consequences for customer risk management?

They are hudge!If you continue to manage your outstandings and your credit analyzes as before, you will be like a collection officer carrying out his scores and reminders on Excel in the age of integrated web credit management solutions: exceeded in efficiency and results.

The great peculiarity of this crisis is its suddenness. A creditworthy business before lockdown begins can be in agony a few months later. In other words, if you set a credit limit and payment terms on the basis of the 2019 balance sheet which has just been published, you are likely to miss the point.

Indeed, mass financial information providers will be lagging behind at least for some time. No algorithm is able to assess in detail the effects of this crisis, which are different for each sector but especially for each company.

As for credit insurers, they are obliged to massively restrict their commitments by making large cuts in the guarantees granted, and this, with few possibilities of doing it on a case-by-case basis. The information collected through the amount of the guarantee thus loses its quality while credit insurance cost increases.

The information obtained directly from customers via telephone follow-up actions in particular and the monitoring of their payment behavior with your company are the first indicators to be taken into account because they are the most immediate, specific and the most factual.

It is therefore the combination between:

- the net cash position before confinement,

- loans obtained,

- receipts from customers,

- the sector of activity and the rate of loss of turnover,

- the amount of fixed charges remaining after the aid which leads to the amount of disbursements,

- the recovery rate following deconfinement,

Evaluate the resilience of a company during an L-shaped crisis

You have to be efficient in credit management. A credit analyst must be able to perform a large number of analyzes in a short time with a reproducible model regardless of the client being assessed.This is why the analysis focuses on simplified information. They can be obtained during a telephone conversation and an analysis of the n-1 financial statements.

- The risk following the crisis is primarily a cash flow risk.

- A second risk that is more present in the background is linked to the profound and lasting changes of this planetary event.

In many cases, it highlights the time lag between the cause (containment) and the effect (possibly negative cash flow) and the better resistance of companies with a high level of liquid current assets (receivables, cash, etc. .).

At the macroeconomic level, it is likely that the increase in insolvencies will be significant, especially in following years.

Conclusion

Assessing the creditworthiness of a company in the short and medium term is essential for any effective risk management.Periods of severe crisis increase the risk of non-payment even though these can be significantly reduced depending on the terms and methods of payment granted and the guarantees obtained.

It is appropriate for each company to define the part of the risk that it accepts to take with each client by applying its credit management strategy which must be rethought and adapted to the situation.

The most important thing is to make choices in full knowledge of the risks involved and according to the objectives and the capacities of your company to absorb a certain level of customer risk.