«Only when the tide goes out do you discover who's been swimming naked.». This somewhat grotesque maxim by Warren Buffet illustrates, however, an inherent reality in times of crisis: if stability frames behavior and conditions it, exceptional situations break these locks and reveals people as they are.

Thus, the current Covid 19 crisis is no exception to the rule.

JI will not discuss the behaviors that pushed individuals to fight for a sack of flour but I will focus on businesses..

Freezing of supplier payments, abuse of exceptional state aid (partial unemployment, etc.) or other attempts to place the financial burden on third parties, often even on their own employees. It may seem surprising that these practices are not applied by the most vulnerable, but rather by financially solid companies where the cynicism of the race for profit (and bonus) at any cost is at the highest.

Under the guise of apparent solidarity, a value which however is usually foreign to them, others are trying to take advantage of the unprecedented situation to launch a free operation aimed at improving their image and gaining market share. After greenwashing, covidwashing has just appeared.

It may seem surprising that these practices are not applied by the most vulnerable, but rather by financially solid companies where the cynicism of the race for profit (and bonus) at any cost is at the highest.

Under the guise of apparent solidarity, a value which however is usually foreign to them, others are trying to take advantage of the unprecedented situation to launch a free operation aimed at improving their image and gaining market share. After greenwashing, covidwashing has just appeared.

Despite the warlike terms usually used to describe the economic world: economic war, competition, target, price battle, sales force, viral marketing (sic), SWOT, etc., the crisis highlights, if it needed to be, the interdependence with each other, with each company with all the others. There does not exist, apart from perhaps the individual organic farmer plowing his fields with the draft horse in Ohio (a visionary), a single company in the world capable of living in autarky. In our organized world which is more globally, only a collective response makes sense. Inward withdrawal and one's own short-term interests are counterproductive in the defense of these same interests.

The acceptance of this reality which is inseparable from a certain humility, collides head-on with the excessive egos and ambitions of company executives and managers. Not easy.

Today, payment behaviors are slipping due to companies whose already tight cash flow tends to crack with the cessation of their activity but especially because of some which, by miscalculation or self-protective reflex block their payments and keep their cash. However, cash in the economy is like blood in the human body: if it does not circulate, it is useless. Its sole vocation is to allow the exchange of goods and services.

The risk of these behaviors is to generate a domino effect leading to cascading failures of businesses.

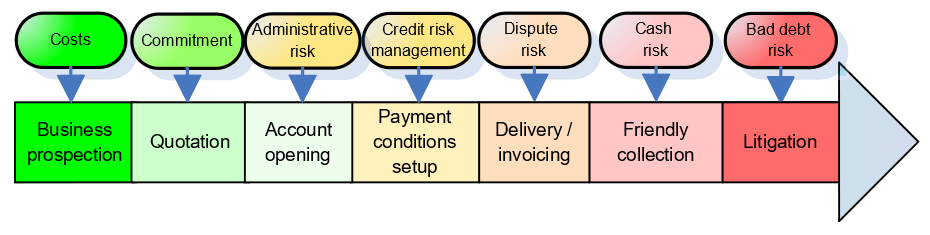

Beyond goodwill, it is necessary to integrate the management imperatives of this "customer financial relationship". It takes place in several stages throughout the sales process.

Ignoring the technicity and complexity of managing receivables is a risk, because without a quality organization, goodwill alone is not enough for a seller to get paid as for a buyer to pay his supplier invoices.

The situation of containment and partial shutdown of companies does not facilitate the quality of this management. Indeed, many operate in degraded mode and have adapted as best they can to telework when possible.

Today even more than yesterday, it is essential to structure the management of its Accounts Receivable, the last decisive step in the operating cycle of companies which determines whether they are paid for their work or whether their debts remain unpaid, first cause of bankruptcies.

Defining a real credit management strategy is therefore essential. For this, a whole ecosystem of specialized companies is at your disposal:

Thus, the current Covid 19 crisis is no exception to the rule.

JI will not discuss the behaviors that pushed individuals to fight for a sack of flour but I will focus on businesses..

Solidarity and Covidwashing

Indeed, if some approached the crisis from a voluntary and positive angle: contribution to compensate for the lack of medical products, protection of their employees and their income (they will be grateful to them), etc., others immediately took egocentric measures dictated by fear by seeking to preserve their interests at all costs whatever are the consequences for the entire economy on which they nevertheless depend.Freezing of supplier payments, abuse of exceptional state aid (partial unemployment, etc.) or other attempts to place the financial burden on third parties, often even on their own employees.

Despite the warlike terms usually used to describe the economic world: economic war, competition, target, price battle, sales force, viral marketing (sic), SWOT, etc., the crisis highlights, if it needed to be, the interdependence with each other, with each company with all the others.

Inter-company credit as a symbol of economic responsibility

Why? Because it’s massive. 600 billion euros in France, much more than bank credit to professionals. Because it also depends on the willingness to pay bills.Today, payment behaviors are slipping due to companies whose already tight cash flow tends to crack with the cessation of their activity but especially because of some which, by miscalculation or self-protective reflex block their payments and keep their cash.

The limits of good intentions

If the will to honorably manage its Accounts Payable is a fundamental element for each company, the fact remains that these exchanges, involving large sums and volumes, between different organizations and with business backgrounds, sometimes complex contracts, are much more demanding than it seems.- Credit analysis: assessment of the buyer's creditworthiness based on the business and related risks (sector, regulatory, policy, foreign exchange, etc.).

- Management of administrative aspects, collection of information necessary for the management and compliance with the regulations in force.

- Contract management (Sales conditions, particular clauses), payment conditions.

- Identification and disputes management so that they can be resolved as soon as possible

- Collection management structured by client typology with recovery scenarios and taking into account the keys to cash collection.

- Management of unpaid invoices and litigation with the appropriate tools (legal actions, insurers, litigation partners, etc.).

- Performance follow-up, then identification of the internal causes of late payments and unpaid debts in order to continuously improve the sales process of your business.

Today even more than yesterday, it is essential to structure the management of its Accounts Receivable, the last decisive step in the operating cycle of companies which determines whether they are paid for their work or whether their debts remain unpaid, first cause of bankruptcies.

Defining a real credit management strategy is therefore essential. For this, a whole ecosystem of specialized companies is at your disposal:

- Financial information providers to track the creditworthiness of your customers. guarantee based on financial report by buyer, de-globalized insurance, single invoice insurance, etc.).

- Consultants and credit management experts.

- Credit management softwares, essential tools as ERP and other accounting softwares are unsuitable for managing customer financial relationships.

- Solutions for financing receivables with or without recourse (factoring, etc.).

- Outsourcing of collection management: you have neither the resources nor the necessary skills to manage Accounts Receivable, specialists chase up your customers on your behalf while taking care to preserve and improve the customer relationship.

- Collection agencies and lawyers to manage litigation requiring legal action.