Risk management or collection? Framework or foundations? Which of these activities is the most important and the noblest?

Some will regard collection as a poor necessity, unlike risk management, which appears more intellectual and technical, apparently only!

Indeed, customer risk management techniques can be complex and difficult to understand for uninformed people: financial analysis, management of credit limits and / or credit insurance contracts, bank coverage (guarantees on first demand, documentary credits, etc. L / C standby), ... each have a specific vocabulary and mechanisms requiring real expertise. As a complex discipline that changes depending on the scope of intervention (export, projects, etc.), customer risk management requires in-depth knowledge of credit analysis and hedging tools.

Cash collection seems more affordable. Indeed, there is no need to understand the multiple clauses and the method of setting up a single risk insurance, for example, to chase up customers.

As a complex discipline that changes depending on the scope of intervention (export, projects, etc.), customer risk management requires in-depth knowledge of credit analysis and hedging tools.

Cash collection seems more affordable. Indeed, there is no need to understand the multiple clauses and the method of setting up a single risk insurance, for example, to chase up customers.

This activity is sometimes carried out by different profiles and by non-specialists (accountants, sales representatives, sales administration, etc.).

However, achieving a good level of performance requires many and varied skills which can sometimes be contradictory. For example, the need to combine accounting rigor in the monitoring of customer accounts and relational flexibility during reminders is not easy while it is essential.

Applying the legislation in force while perceiving what must be strictly applied (respect of maximum payment terms allowed for example) and what can be ignored or canceled (late payment penalties) is another. On this subject, read our many business tutorials on B to B cash collection which illustrate the difficulty of this activity located at the heart of the commercial relationship but dealing with financial aspects as well as customer satisfaction (dispute management, etc.). More affordable but requiring great finesse to achieve good performance. A collection manager must be able to manage a large volume of accounts receivable and invoices, improving by his action the cash flow and profitability of his business, as well as customer satisfaction.

Digital collection also requires good mastery of business software, knowing how to interact with them, and having a significant capacity to analyze data in order to effectively manage a large volume of receivables and customers.

So should we oppose these two activities? Should we favor one over the other? These questions lead to ask another, more fundamental, about the purpose of credit management. What is the ultimate objective of this function in the company?

Some credit managers will assert that their objective is to assess and then control customer risk with the appropriate tools and using their skills and technical expertise. Certainly, but here they confuse the end and the means. Risk management is not an end in itself but only a means to achieve the company's objective of developing its turnover and getting paid on time.

Risk management and collection are therefore complementary and intrinsically linked, feeding into each other. For example, the collection scenario applied to a customer could be dynamically adapted according to its risk profile. The collector will thus be particularly attentive during the reminders carried out with a risky client and in his follow-up.

In addition, he or she will be able to observe any deterioration in a buyer's payment behavior, which is often the first warning of a company's financial difficulties, and will thus contribute to a fair assessment of the risk of non-payment. It is therefore in its entirety that a customer account must be understood. In addition, credit analysis tools are mainly based on information from the past, in particular financial statements, which can quickly appear to be out of date given the acceleration of economic times. Taking into account the situation of the customer account from a debt collection point of view is therefore all the more relevant as it is current.

Indeed, credit management includes many activities behind the company's sales process: risk, customer accounting, amicable collection and dispute management, litigation and performance management, improvement of internal business processes. All these activities tend towards a single fundamental objective: to develop the turnover while being paid quickly and well. There is no more or less noble or important part because each part needs the other to function.

This diversity is the richness of the profession of credit manager and embracing its multiple facets is the surest way to act positively for your company, without blinders and with a lot of foresight and discernment.

Some will regard collection as a poor necessity, unlike risk management, which appears more intellectual and technical, apparently only!

Indeed, customer risk management techniques can be complex and difficult to understand for uninformed people: financial analysis, management of credit limits and / or credit insurance contracts, bank coverage (guarantees on first demand, documentary credits, etc. L / C standby), ... each have a specific vocabulary and mechanisms requiring real expertise.

This activity is sometimes carried out by different profiles and by non-specialists (accountants, sales representatives, sales administration, etc.).

However, achieving a good level of performance requires many and varied skills which can sometimes be contradictory. For example, the need to combine accounting rigor in the monitoring of customer accounts and relational flexibility during reminders is not easy while it is essential.

Applying the legislation in force while perceiving what must be strictly applied (respect of maximum payment terms allowed for example) and what can be ignored or canceled (late payment penalties) is another. On this subject, read our many business tutorials on B to B cash collection which illustrate the difficulty of this activity located at the heart of the commercial relationship but dealing with financial aspects as well as customer satisfaction (dispute management, etc.).

Some credit managers will assert that their objective is to assess and then control customer risk with the appropriate tools and using their skills and technical expertise. Certainly, but here they confuse the end and the means. Risk management is not an end in itself but only a means to achieve the company's objective of developing its turnover and getting paid on time.

Risk management and collection are therefore complementary and intrinsically linked, feeding into each other. For example, the collection scenario applied to a customer could be dynamically adapted according to its risk profile. The collector will thus be particularly attentive during the reminders carried out with a risky client and in his follow-up.

In addition, he or she will be able to observe any deterioration in a buyer's payment behavior, which is often the first warning of a company's financial difficulties, and will thus contribute to a fair assessment of the risk of non-payment.

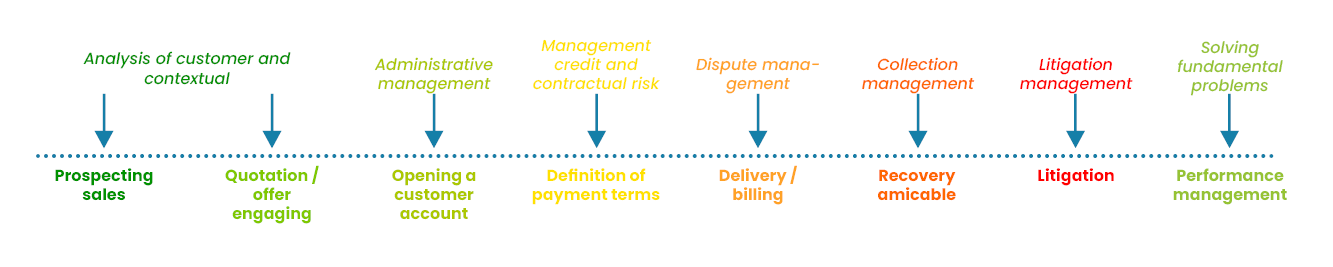

Credit management and quote to cash process

The credit manager is involved in the entire Quote to Cash process of the company. Each step is essential for the smooth running of the entire process.Indeed, credit management includes many activities behind the company's sales process: risk, customer accounting, amicable collection and dispute management, litigation and performance management, improvement of internal business processes. All these activities tend towards a single fundamental objective: to develop the turnover while being paid quickly and well. There is no more or less noble or important part because each part needs the other to function.

This diversity is the richness of the profession of credit manager and embracing its multiple facets is the surest way to act positively for your company, without blinders and with a lot of foresight and discernment.